Whole life insurance is one of the types of life insurance. It is designed to help customers mitigate risks in life, providing financial support in case of unfortunate events such as death due to poverty or unforeseen circumstances. To understand in detail what whole life insurance is and its various types, please read the following article.

1. What is Whole Life Insurance?

Whole life insurance is used when the insured person passes away within a specific period. In such cases, the insurance company will pay a sum to the beneficiary if the insured person dies while the insurance policy is still valid. If the policy matures, and the insured person is still alive, the insurance company is not obligated to make any payments. Even if the insured person dies one day after the policy matures, the company’s payment responsibility ceases to exist.

2. Characteristics of Whole Life Insurance

Whole life insurance has the following basic characteristics:

- It has a specified term.

- Premiums and insurance benefits are lower than term life insurance.

- The premium payment period may be shorter than the contract term.

- It has no cash value like whole life insurance, and there is no surrender value.

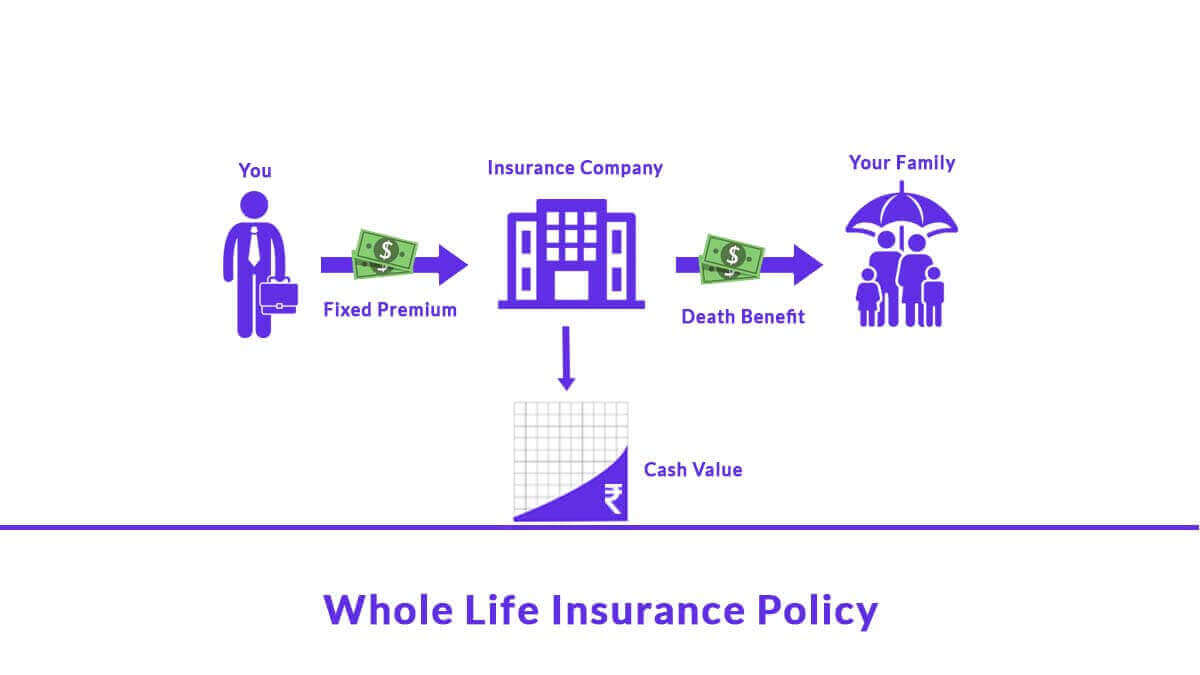

- There is no savings element, as whole life insurance only pays out if the insured person dies during the coverage period. If the contract matures without any insured event occurring, no payment or refund will be made.

In summary, whole life insurance is not intended for savings but rather to protect against risks.

3. Conditions for Claiming Whole Life Insurance Benefits

The conditions for claiming benefits from whole life insurance depend on the terms of the contract. If the insured person dies while the whole life insurance contract is still valid, the insurance company will make the payment. Conversely, if the insured person is still alive at the contract maturity date, both parties terminate the contract without any payment.

4. Types of Whole Life Insurance

4.1 Fixed Whole Life Insurance

Fixed whole life insurance is a traditional form of insurance with the lowest premiums and straightforward terms. Premiums and insurance amounts during the effective period remain unchanged. If the insured person dies during the policy term, the company pays the insurance amount to the family. There is no value accumulation, and it does not provide a refund at maturity. Fixed whole life insurance aims to protect financial stability against risks without a savings component. Therefore, there is no refund when the contract expires, meaning you won’t get money back as in traditional life insurance. However, this contract serves as a solution to help the family pay off any outstanding debts of the insured person (if any) upon their death.

Key features of fixed whole life insurance:

- Low insurance premiums.

- Specific insurance period.

- Fixed premiums and insurance amounts.

- No cash value or refund.

- No payment upon contract expiration if the insured person is alive.

- The contract becomes invalid if premiums are not paid after the grace period.

4.2 Renewable Whole Life Insurance

In this contract, the insured person has the right to request renewal on the expiry date without providing evidence of current health status. Premiums will increase compared to the old contract and depend on the insured person’s age at the time of renewal. The renewable age limit for whole life insurance is typically 65. If the insured person reaches the age of 65, renewal is no longer possible.

Key features of renewable whole life insurance:

- Can renew the contract without proof of health status.

- Policyholder can cancel or renew the contract at the end of the term.

- Premiums will increase based on the insured person’s age at the time of renewal.

4.3 Convertible Whole Life Insurance

With this type of insurance, the insured person can convert part or all of the existing whole life insurance contract into a permanent life insurance or a mixed life insurance contract while the policy is still valid. The annual insurance premium depends on the features of the new insurance contract and the age of the insured person. To complete the conversion procedure, the insured person must pay an additional conversion fee to the insurance company.

Key features of convertible whole life insurance:

- Can convert to a permanent life insurance or mixed life insurance contract while the original contract is valid.

- Can choose to convert part or all of the contract.

- Higher insurance premiums and conversion fees.

4.4 Decreasing Whole Life Insurance

Decreasing whole life insurance is often used to ensure that outstanding debts are gradually paid off in case the insured person dies. It is commonly associated with installment purchases such as real estate, vehicles, bank loans, etc. The insurance amount of the decreasing whole life insurance contract decreases over time, as stipulated in the contract. This amount corresponds to the remaining debt of the insured person.

Key features of decreasing whole life insurance:

- Premiums are usually lower and more fixed than fixed whole life insurance.

- The mandatory premium payment period may be shorter than the entire contract period. In the final stages of the contract, the insured person may not have to pay premiums.

- The insured person receives a minimal amount of money near the end of the contract compared to the total insurance amount when signing the contract.

4.5 Increasing Whole Life Insurance

Increasing whole life insurance is designed to counteract the effects of inflation. In times of inflation, the real value of the insurance sum of the contract will decrease over a specific period. According to this contract, the annual insurance sum will increase by a certain percentage. For example, when signing the contract, the insurance amount is 100 million, and the contract specifies that this amount will increase by 10% each year. The contract period is 15 years. Suppose the insured person dies after 5 years from the contract signing date. In that case, the beneficiary will receive an amount of 150 million Vietnamese dong.

Some insurance companies also offer contracts with short renewal periods. The insurance amount will increase after each renewal.

Key features of increasing whole life insurance:

- The insurance amount within the contract period may increase without evidence of health status.

- Premiums also increase with the insurance amount during renewal.

- Premiums are usually higher than those of fixed whole life insurance.

- To continue the contract, the age of the policyholder should not exceed 60-65.

4.6 Family Income Whole Life Insurance

In the event of the death of the breadwinner in the family, this type of insurance supports the family by providing a replacement income for a specified period. According to the contract terms, if the insured person dies and the contract is still valid, the insurance company will periodically pay a sum until the end of the contract or until the beneficiary reaches a certain age. In many countries worldwide, families receiving periodic payments from this type of contract do not have to pay personal income tax on that amount. This humanitarian approach encourages people to participate in insurance.

The premium for this type of contract is relatively low. As the contract approaches maturity, the amount paid to the insured person decreases. If the contract has reached the end of its term and the insured person is still alive, the insurance company will not have to pay any amount.

Moreover, many companies design family income whole life insurance with an increasing element. This is to compensate for the impact of inflation, ensuring that the real value of the benefit is maintained over time.

Key features of family income whole life insurance:

- The insurance company pays periodically until the end of the contract or until the beneficiary reaches a certain age.

- Relatively low insurance premiums.

- The gradually paid amount is considered tax-free income.

5. When to Buy Whole Life Insurance

You may consider purchasing whole life insurance in the following cases:

- You are the breadwinner, the primary source of income in the family.

- You are concerned about your health and life.

- You want a low-cost contingency plan for financial risks in case of unexpected events.

- You have savings in the bank and can combine it with whole life insurance to provide long-term income higher than investment-based insurance. The risk of losing money in this type is almost non-existent.

By now, you should have a comprehensive understanding of what whole life insurance is. Participating in whole life insurance or any other type of insurance is your decision. Take the time to thoroughly research various insurance options and consider personal and family factors to choose the most suitable insurance package.

Cre: Zhu/fincash.com