Currently, there are many types of insurance, from domestic insurance to international insurance. Surely everyone has heard of non-life insurance and has some understanding of it. However, when it comes to non-life insurance, many people are still confused about it. Here, MFast will help you understand more about non-life insurance and what to consider when buying this type of insurance.

1. Non-life insurance concept

Non-life insurance is a voluntary insurance product aimed at individuals and entities related to individuals, such as health, goods, accidents, for the purpose of insuring against these risks. Therefore, each person participating in non-life insurance usually pays a one-time insurance premium and is required by the insurance company to pay and compensate within the specified period (1 to 2 years) if there are risks of disability, death, loss, damage, accidents during the insurance period. If there are no risks during the insurance period, when the contract is terminated, the rights and obligations between the parties will expire, and the participant will not recover their insurance money. Non-life insurance includes activities such as health and accident insurance, fire and explosion insurance, aviation insurance, motor vehicle insurance, cargo insurance, etc.

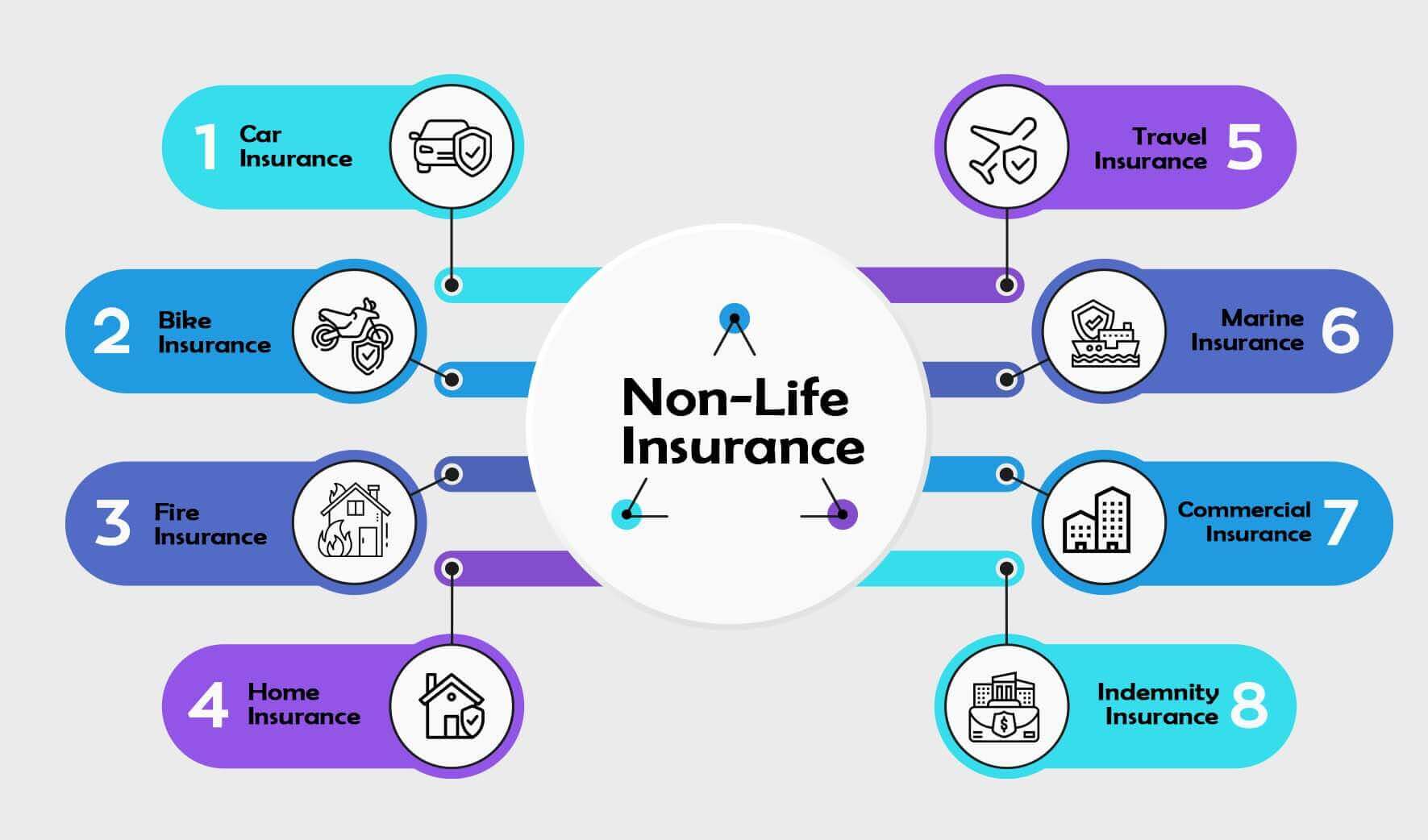

2. Types of non-life insurance

Currently, in the market, non-life insurance is divided into various types depending on the insurance company you sign up with. Typically, non-life insurance types are divided into the following categories:

2.1. Health and personal accident insurance:

This is a type of insurance for cases where the insured person encounters unforeseeable risks leading to serious consequences such as disability, illness, accidents, or even death. Insurance companies will have to pay an insurance amount according to the signed contract.

2.2. Business interruption insurance:

This is a type of insurance specifically for businesses, companies, to prevent risks to assets during business and production. The enterprise will have to set aside an insurance amount equivalent to the agreed-upon amount in the contract if the company encounters any risks.

2.3. Property insurance and damage insurance:

This insurance is specifically for the personal property of the insured, such as tangible assets, valuable documents, property rights, or money, in case of unforeseen incidents.

2.4. Aviation insurance:

This type of insurance is for individuals and goods participating in air transportation. If the insured person encounters risks during the flight, they will be compensated an amount equivalent to the insurance package specified in the contract (Note: aviation insurance does not cover goods and individuals).

2.5. Motor vehicle insurance:

This type of insurance is specifically for motor vehicles when encountering unforeseen circumstances or accidents. This insurance protects both individuals and vehicles and cargo on motor vehicles.

2.6. Fire and explosion insurance:

This type of insurance is used to compensate for the damages that the insured person encounters, affecting the property or life of individuals when facing incidents related to fire or explosions.

2.7. Road, sea, river, rail, and air cargo insurance:

This type of insurance is for various types of goods during transportation by road in case of any unforeseen events or accidents (Note: this type of insurance is only for goods).

2.8. Hull insurance and liability of the shipowner:

This type of insurance compensates for damages to the ship’s hull and unexpected risks, sudden incidents that the shipowner must bear the cost of third-party damage during the operation of the ship.

2.9. Credit and financial risk insurance:

This type of insurance ensures loans at the bank in case of unforeseen risks that cannot repay the debt.

3. Reasons to choose non-life insurance

As a participant in insurance, what do you get by choosing non-life insurance:

Better risk management: No one wants to encounter risks in life, but surprises happen that we cannot predict. So participating in non-life insurance is a way to protect your life and property, helping you minimize the damage you may encounter in accidents.

Compensation, economic assistance: If you participate in non-life insurance, when encountering unexpected incidents leading to significant damage to your property and health, the insurance company will help you pay a certain amount to reduce the damage caused by the accident.

Peace of mind: When participating in non-life insurance, you will be carefully advised on suitable insurance packages, signing transparent contracts from insurance companies. So, whether participating in production activities or just going out, you will be more reassured because you have non-life insurance to protect your health and property.

4. Things to note when participating in non-life insurance

Before deciding to participate in non-life insurance, you need to note the following:

Regarding the purpose: Non-life insurance aims to protect participants from unexpected risks related to property, individuals, and human responsibilities.

Regarding accumulation: There is no accumulation, and after the contract ends, the customer will not receive the premium back.

Regarding the contract period: Participants usually pay for 1 to 2 years, or even a shorter time.

Regarding the premium payment time: Participants in insurance will pay the entire amount once after signing the contract. If you continue to sign the contract later, you will pay premiums for the following years according to the contract.

Regarding factors affecting the decision to choose insurance packages: Participants in non-life insurance usually pay attention to factors such as insurance coverage, risk probability, and the insurance amount.

Regarding the beneficiary: The beneficiary will be the victim of the incident, whether directly or indirectly.

Regarding the case of benefit payment: Participants will only receive benefit payments when there is a risk.

Non-life insurance is a necessary tool for everyone, and it needs to be carefully researched and selected appropriately. This article has clearly explained non-life insurance and what to consider when buying.

Cre: Maria Jane/ mfast